Gold has firmly re-entered the global investment conversation. In 2025, the metal delivered an exceptional return of 64% (USD), placing it among the strongest-performing major asset classes over the period.

This resurgence has been driven by far more than short-term price momentum. Instead, it reflects a convergence of structural forces that have reshaped how investors and institutions think about risk, monetary stability, and long-term capital preservation.

ADVERTISEMENT

CONTINUE READING BELOW

Elevated geopolitical tensions, rising sovereign debt burdens, persistent inflationary pressures, and growing concerns around currency debasement have collectively reinforced gold’s role as a trusted store of value.

While gold has always been viewed as a defensive asset, the current environment has highlighted its relevance as a strategic allocation within diversified portfolios, rather than a tactical or opportunistic trade.

Central banks, reserve shifts, and the structural case for gold

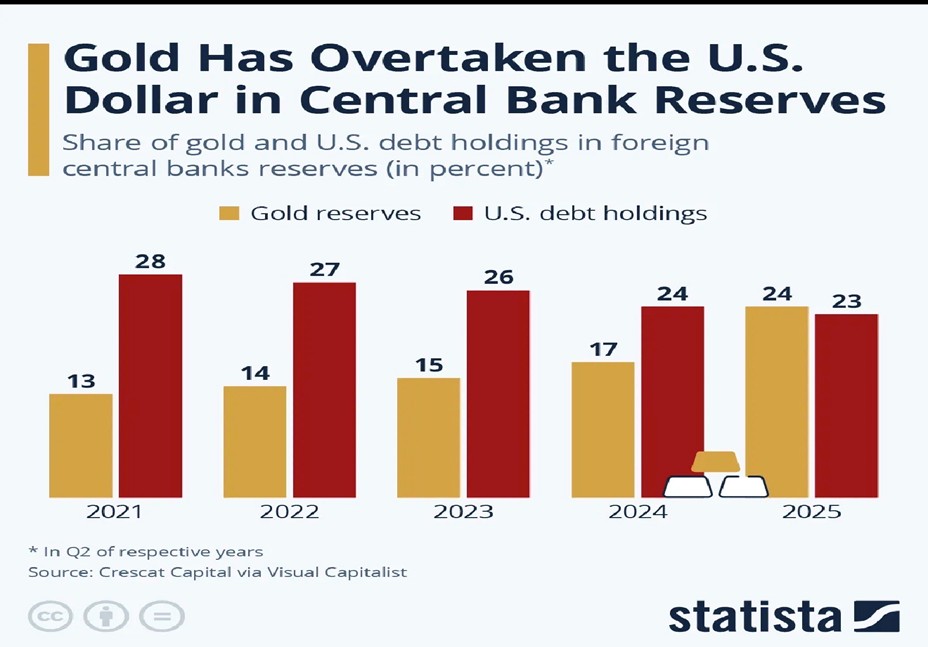

One of the most powerful forces underpinning gold’s strength has been sustained and broad-based central bank demand. For the first time since 1996, foreign central banks now hold more gold in their reserves than US treasuries, marking a symbolic and structural shift in global reserve composition.

This transition reflects a gradual diversification away from dollar-denominated assets and towards hard assets that are not directly linked to any single country’s fiscal or monetary policy.

Rising US debt levels, expanding budget deficits, and the long-term implications of prolonged monetary accommodation have encouraged reserve managers to reassess concentration risk within their portfolios.

Central bank buying has been both consistent and sizeable. In 2022 alone, official sector purchases reached a record 1 136 tonnes, with 2023 and 2024 maintaining historically high levels of accumulation.

This trend is particularly notable given that nearly one-fifth of all the gold ever mined is now held by central banks, highlighting the metal’s enduring role in the global financial system.

The distribution of these reserves further reinforces gold’s importance. The US and Europe collectively account for more than 60% of global official gold holdings, reflecting decades of accumulation and the strategic value assigned to gold as a reserve asset.

At the same time, emerging economies have become increasingly active buyers. China added approximately 331 tonnes between 2019 and 2024, lifting its total holdings to around 2 280 tonnes, while countries such as India, Poland, and Turkey have also made meaningful additions.

This widespread institutional demand has been a key contributor to gold reaching record highs in 2025 and suggests that the current rally is supported by long-term structural flows rather than speculative excess.

Gold compared to US equities: Performance cross time horizons and market cycles

When comparing gold with equities, particularly US equities, recent performance differences must be viewed within the context of time horizons and market cycles. Over shorter periods, gold has outperformed meaningfully.

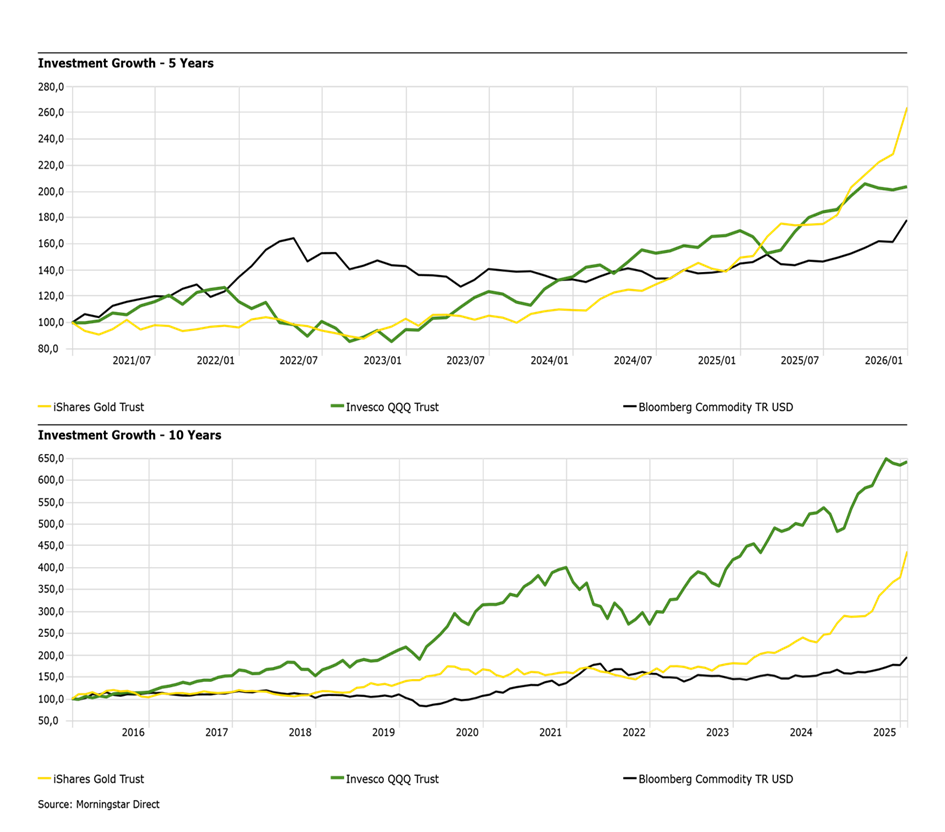

Over the past five years, gold delivered annualised returns of approximately 21.43% (USD), compared with around 15.27% (USD) for the Nasdaq. These results reflect an environment characterised by elevated inflation, aggressive monetary tightening, geopolitical uncertainty, and heightened volatility – conditions under which gold has historically performed well.

However, as the investment horizon extends, equities increasingly demonstrate their long-term growth advantage. Over a 10-year period, gold returned approximately 15.72% (USD) per annum, and over 15 years around 8.95% (USD) per annum.

Over the same periods, the Nasdaq delivered annualised returns of approximately 20.44% (USD) and 18.44% (USD), respectively. On a cumulative basis, this difference becomes even more pronounced. Over 15 years, an investment in US equities would have grown by approximately 541% (USD), compared with around 314% (USD) for gold.

An initial investment of USD 10 000 would therefore have increased to approximately USD 64 100 in US equities, compared with roughly USD 41 000 in gold. These outcomes highlight the compounding power of equities, driven by earnings growth, innovation, productivity improvements and reinvested dividends.

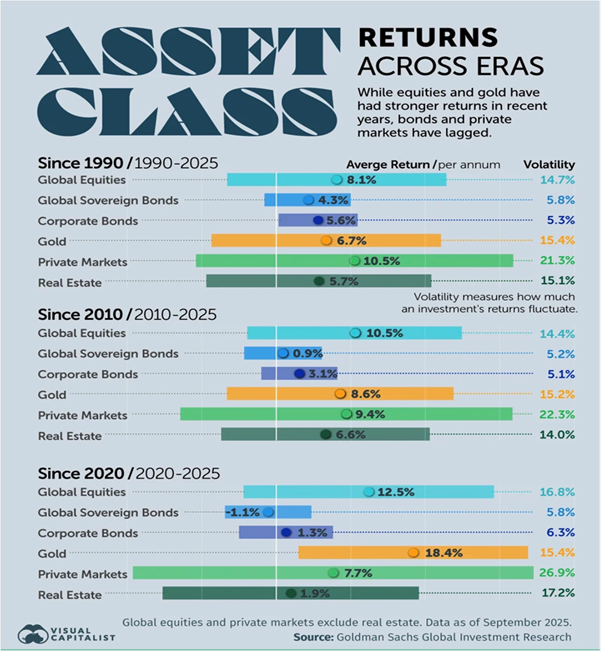

Broader asset class data reinforces this perspective. Since 1990, global equities have delivered average annual returns of approximately 8.1% (USD), compared with gold’s 6.7% (USD).

From 2010 to 2025, global equities returned approximately 10.5% (USD) per annum, while gold returned around 8.6% (USD) per annum. More recently, from 2020 to 2025, gold has outperformed with annualised returns of approximately 18.4% (USD), compared with global equities at roughly 12.5% (USD).

These shifts illustrate that leadership rotates over time, shaped by changes in inflation, interest rates, growth expectations, and investor confidence.

ADVERTISEMENT:

CONTINUE READING BELOW

The below graph illustrates the total return of gold compared to the Nasdaq over a five- & 10-year periods:

Risk, drawdowns, and the case for long-term diversification

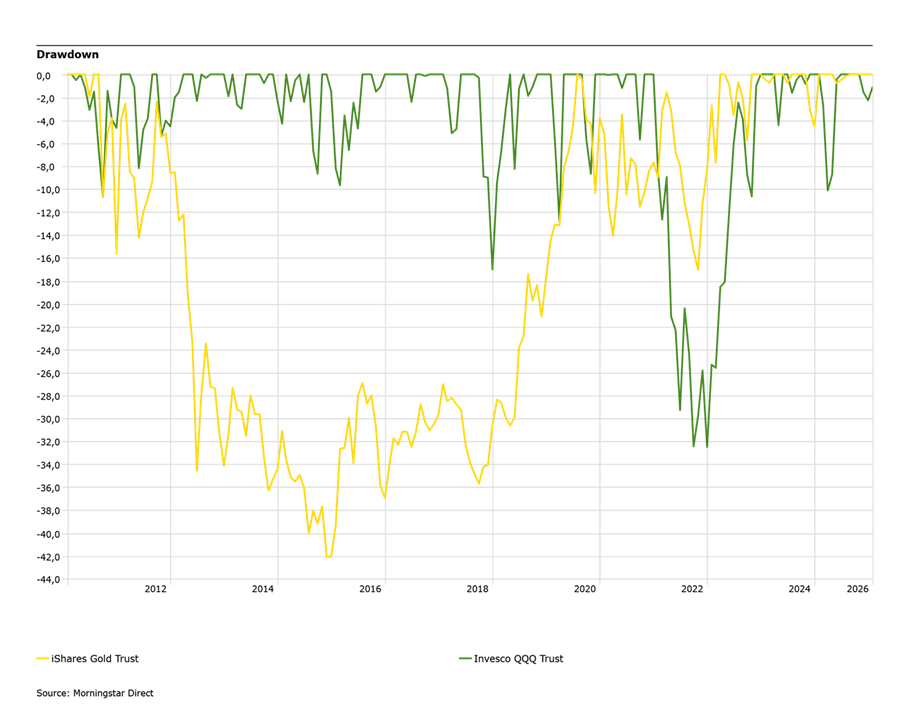

An equally important consideration when evaluating gold and equities is risk, particularly in the form of drawdowns. While equity markets – especially technology-heavy indices – are often perceived as inherently riskier, gold has also experienced significant drawdowns during past cycles, in some cases exceeding 40%.

No asset class is immune to volatility, and periods of strong performance are often followed by extended phases of consolidation or decline. The distinction lies not in avoiding drawdowns entirely, but in how different assets behave relative to one another during periods of stress.

Gold has historically provided resilience during inflationary environments, monetary policy shocks, and periods of geopolitical uncertainty, often acting as a stabilising force when risk assets struggle.

Equities, by contrast, tend to experience sharper short-term volatility but have consistently been the primary engine of long-term wealth creation. This difference in behaviour is precisely why both assets play complementary roles within diversified portfolios.

Attempting to rotate entirely into a single asset class based on recent performance increases the risk of untimely decisions and foregone long-term returns.

The most resilient portfolios are therefore built over a long-term perspective rather than around short-term forecasts. A diversified, actively managed portfolio allows investors to participate in growth during favourable environments while maintaining exposure to defensive assets that can help manage risk during periods of uncertainty.

The objective is not to maximise returns over one or two years, but to compound wealth steadily over decades by combining assets with different return drivers, volatility profiles, and responses to changing market conditions.

The below graph illustrates the drawdown levels of gold compared to the Nasdaq:

Gold’s strong performance in recent years has been both notable and well supported by structural shifts in central bank behaviour, elevated uncertainty, and evolving monetary dynamics.

At the same time, equities remain the most effective long-term wealth-building asset, underpinned by innovation, earnings growth, and global economic expansion.

The long-term evidence is clear: no single asset class consistently outperforms across all environments. Investors are best served by maintaining perspective, avoiding the temptation to chase recent performance, and constructing portfolios that are diversified, actively managed, and aligned with long-term objectives.

By investing across cycles rather than reacting to them, portfolios are better positioned to manage risk, navigate volatility, and deliver sustainable long-term outcomes.

The below diagram illustrates the return of different asset classes since 1990: