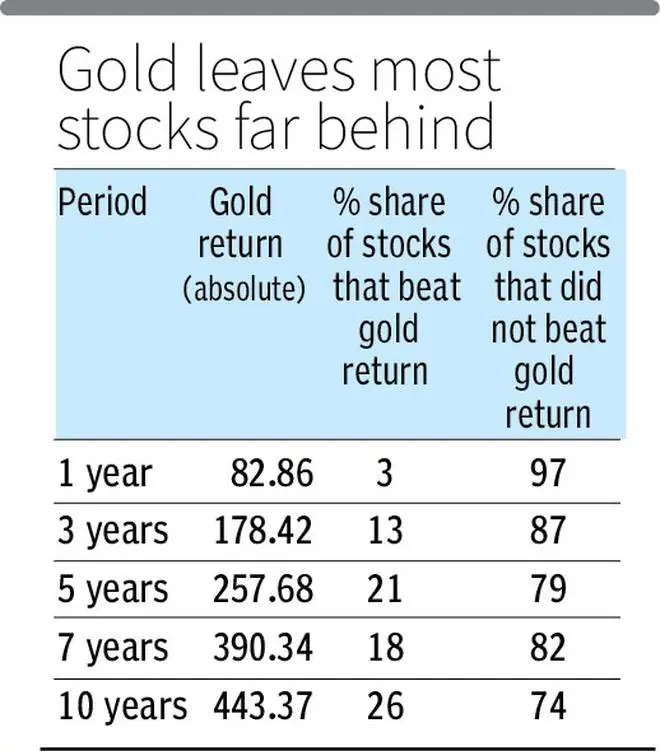

If Indian equities are supposed to reward patience, gold, often lampooned as a ‘dead’ asset, has spent the last decade mocking that promise. In the one year to March 13, 2026, gold (MCX spot prices) returned 82.86 per cent. Out of roughly 1,134 NSE-listed stocks with sufficient trading history, only 37 or 3 per cent beat it. That means 97 per cent did not. But the real insult lies in the longer periods where equity investors usually demand respect for their endurance. Over three years, gold returned 178.42 per cent and only 13 per cent of stocks beat it. Over five years, it returned 257.68 per cent and just 21 per cent beat it. Over seven years, only 18 per cent got past gold’s 390.34 per cent return. Even over ten years, after all the sermons on compounding, discipline and staying invested, only 26 per cent of stocks managed to outperform gold’s 443.37 per cent gain.

So yes, India’s Dalal Street may have built an equity culture after Covid. But the precious metal has built a case file of crushing performance. This is what makes the old line about the Indian housewife being the world’s best fund manager so irritatingly durable. While the formal investor learnt to say SIP, smallcap, tactical allocation and buy-on-dips, she kept buying gold. No earnings calls. No management guidance. No quarterly disappointment. Just a dull-looking metal quietly doing the one thing equity markets never stop claiming to do for investors: preserve purchasing power and occasionally embarrass consensus.

And no, this is not merely one freak year of missiles, oil tanker worries and safe-haven panic. The yearly cuts show that gold has repeatedly been a difficult hurdle for stocks even when its own annual return was not spectacular. In the latest one-year period ended March 13, 2026, gold rose 82.86 per cent and only 3 per cent of stocks beat it. In the 2025 cut, gold returned 32.57 per cent; still, 82 per cent of stocks failed to beat it. In 2023, gold returned only 8.59 per cent, yet 63 per cent of stocks still could not get past it. In 2020, gold rose 29.9 per cent and a crushing 96 per cent of stocks lagged it. In 2019, gold’s return was just 6.57 per cent, and yet 84 per cent of stocks still failed to beat it. That is the larger embarrassment. Gold did not need to be brilliant every year. The stock universe merely needed to be ordinary, volatile or badly distributed. Equity bulls can, of course, point to the friendlier windows. In the 2021 cut, when gold returned 5.54 per cent, 94 per cent of stocks beat it. In 2024, with gold up 14.85 per cent, 75 per cent did. In 2017 and 2018 too, equities did better on breadth. But that actually strengthens the point. Equity culture remembers the party years and markets them as destiny. Gold waits for the more disorderly years and keeps winning enough of them.

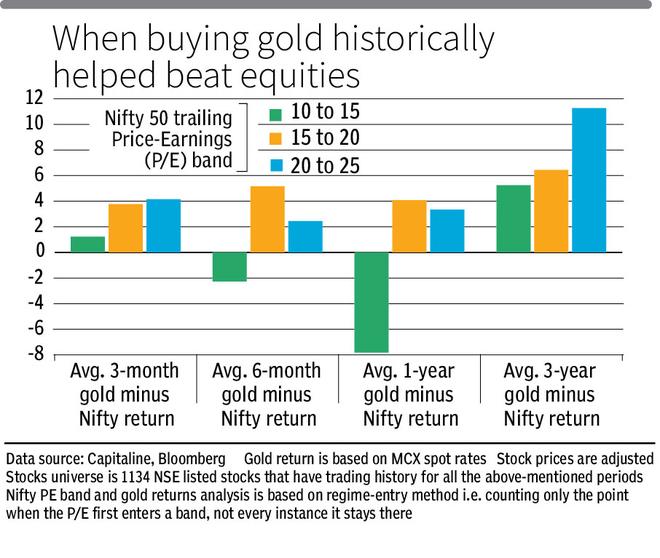

The forward-looking clue in data is just as awkward for equity purists. When starting Nifty 50 valuations are not especially cheap, gold has often done well relative to the index. When the Nifty 50 P/E (price to earnings) starts in the 20-25 band, gold beats the Nifty 50 by an average 11.27 percentage points over three years. In the 15-20 band, it beats by 6.44 points. Even in the 10-15 band, it still edges ahead over three years. Gold’s own average three-year

returns across starting valuation bands are hardly meek either — 61.52 per cent from the 10-15 band, 46.31 per cent from 15-20 band, 48.05 per cent from 20-25 band.

The joke, then, is on modern portfolio snobbery. The asset long treated as backward, unproductive and a little too attached to family lockers has spent years exposing just how few stocks actually deliver the heroic long-term story investors are sold. Gold may not produce cash flows. But it has produced something just as valuable over the past decade — discomfort for anyone who thought equities would easily leave it behind.

All this does not mean investors should dump equities and marry bullion. It simply means gold has historically looked most useful when fear is rising, liquidity is uncertain, and equities are not entering from obviously cheap valuations. In plain English, when the market is expensive, the world is noisy and everyone is pretending this is normal, gold deserves more respect than the average stock bull likes to give it.

Published on March 14, 2026