The question of whether the global bull market will continue came up for discussion in Anchor Asset Management’s most recent quarterly market outlook.

“The bull market has been running for some time, and we expect it to continue, though with more moderate returns,” says Anchor founder and co-CEO Peter Armitage.

Listen: It’s a bull market, don’t fight it

“We expect returns to be closer to the average of the past 10 to 20 years, rather than the 20% seen in the last year or two.

“The weaker dollar, declining interest rates and substantial AI capital expenditure have been highly stimulatory for the US economy.

“Added to that, some of the positive effects of recent Trump policies have also supported economic growth,” says Armitage.

“However, we remain cautious with new investments because valuations are high. While we expect earnings to grow by around 10% to 15% per annum over the next three years, overall market returns are likely to be slightly lower than that.

“Companies are being punished more heavily for earnings misses, largely due to their already elevated valuations,” he adds, noting yet again that SA shares are offering relatively good value.

Listen: SA Equities: Implications of US rate cuts for emerging markets

Anchor’s investment team says it is not expecting massive returns globally. Portfolio manager Liam Hechter says the firm remains positive on SA equities.

“Bonds offer around 9%, which looks attractive if the currency remains broadly stable, especially when compared to global yields of 4%,” says Hechter.

“Listed property offers even higher yields, around 11%, as falling bond yields have made property dividends more appealing. The post-Covid lease reversion cycle appears to be ending, and property companies are expected to grow earnings by about 4% to 6%, with dividend yields between 7% and 10%.”

Hechter adds that local alternative funds “can also provide a complementary return profile”.

ADVERTISEMENT

CONTINUE READING BELOW

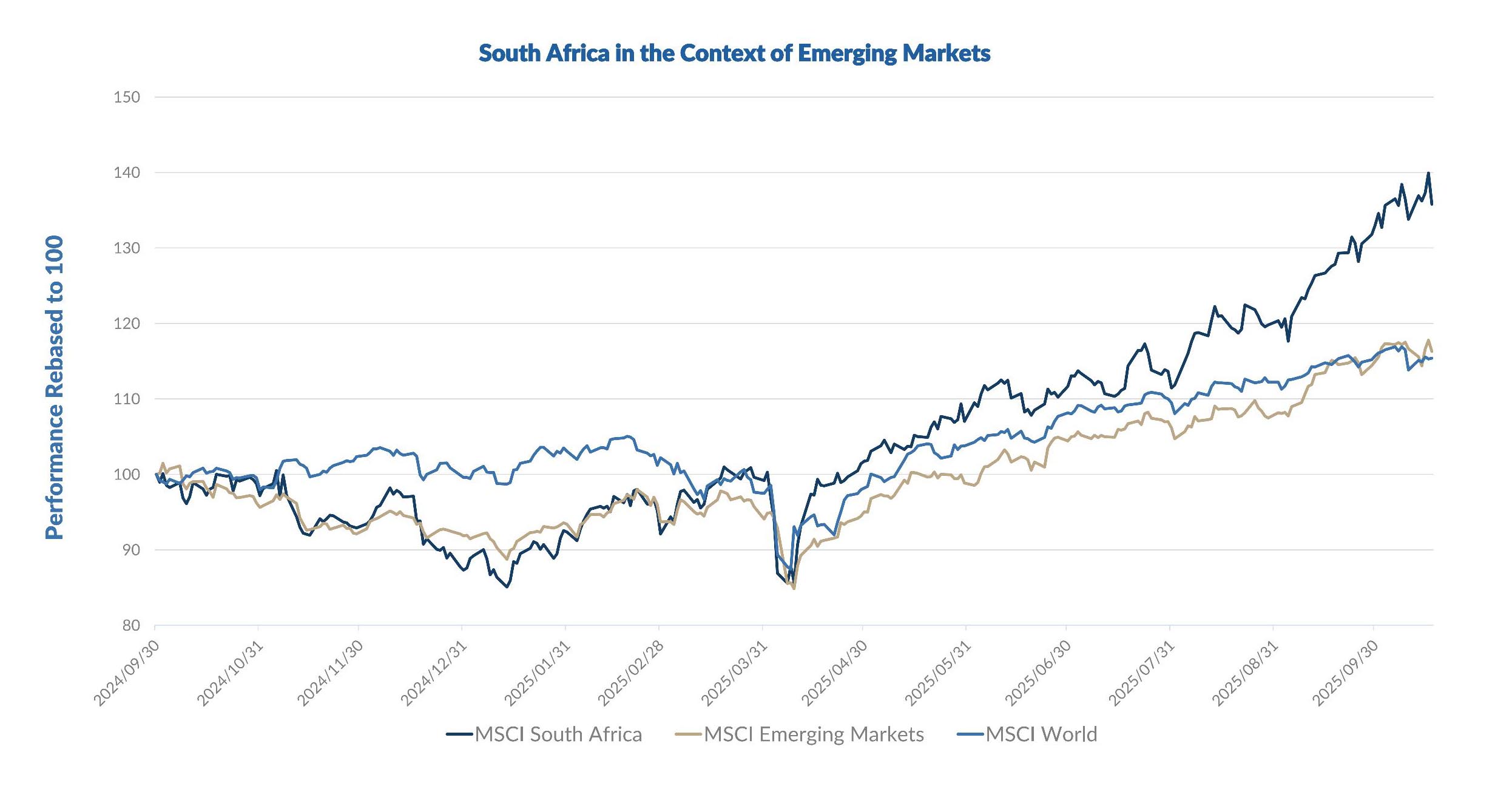

He describes the run on the JSE during the past five years as a “stealth bull market” and highlights the particularly good performance of the JSE compared to other emerging markets since the low of March 2025.

JSE outperforms other emerging markets

Source: Bloomberg

“The JSE has performed surprisingly well, keeping pace with the S&P 500 over the past decade. Although the ride has been more volatile, South African investors have been rewarded for their patience,” says Hechter.

“A combination of a low earnings base created during Covid and attractive valuations has supported strong returns. This highlights the importance of not exiting assets during difficult periods – a common tendency among investors.

“Despite geopolitical tensions, domestic social unrest and sluggish economic growth, many SA companies have adapted and grown successfully. Shoprite, for example, has expanded its market share in a stagnant environment, demonstrating how resilient businesses can thrive even amid low growth.”

Listen/read: ‘An outstanding performance from Team Shoprite’

Hechter bemoans the fact that the JSE has become increasingly concentrated in recent years, particularly within basic materials and precious metals, which now drive a large portion of returns.

“This concentration introduces additional complexity to asset allocation and forecasting, as movements in platinum group metals (PGMs) and gold prices heavily influence overall performance.

“Over the past five years, SA markets have experienced distinct phases. For investors focused on quality, compounding businesses, the most significant development was the shift in the political environment over the past year.

“While progress on structural reforms has been slower than expected, the direction remains positive. Notable improvements include better management of the energy grid since the peak of load shedding in 2022 to 2023, and early progress in resolving Transnet’s logistical bottlenecks,” he says.

Read:

2025 has been kind to the JSE – but not to most shares

SA to miss growth target on slow reforms – Moody’s

Turnarounds at Eskom and Transnet not yet showing in GDP figures

ADVERTISEMENT:

CONTINUE READING BELOW

The JSE proved over the last few years that SA continues to benefit from being a major commodity exporter.

“It positions the JSE – and local investors – well when emerging markets are in favour,” says Hechter.

“This global tailwind, combined with gradual domestic reforms, has created a supportive backdrop for local assets.

“Gold has become a major part of the JSE, rising from just over 2% of the index in 2022 to more than 15% now. This sharp increase has boosted returns but also raised volatility and forecasting risks.

“PGMs have also gone through a full boom-and-bust cycle, further illustrating how cyclical the local market can be,” according to Hechter.

Read:

Gold and platinum shares steal the show as JSE cracks new high

Gold shares have run hard but are still cheap

From the beginning of 2025 to end September, SA equities are up around 35%, driven primarily by gold and other precious metals.

Big index components such as Gold Fields, AngloGold Ashanti and PGM producers have more than doubled, contributing the majority of the index’s gain.

Gold Fields and AngloGold Ashanti

Outside of these, market breadth has been limited, with the rest of the JSE up only about 8%.

“Given this concentration, we expect the best returns to come from the more diversified, domestically focused sectors in the coming year,” says Hechter.

“We remain constructive on South Africa’s prospects. The stronger currency, solid bond performance and rising tax revenues from commodities are all positive indicators.

“However, risks remain, including political uncertainty ahead of the ANC leadership race and upcoming local elections, as well as heightened global geopolitical volatility. Investors should stay alert to these potential disruptions.”

ADVERTISEMENT:

CONTINUE READING BELOW

Outlook

Anchor’s quarterly outlook – tagged ‘Where the money will be made’ – tries to identify where investors can find the best returns over the next 12 months.

This time it notes that the banking sector is still offering value.

Dividend yields are comparable to the yield on 10-year government bonds and earnings growth is expected to range between 8% and 13%.

“Banks are trading at attractive valuations relative to history. Among the more compelling ideas, Absa stands out as an undervalued turnaround story (under new management), offering strong dividends and double-digit earnings potential,” says Hechter.

“Pairing it with a high-quality grower like Capitec – which trades at a premium but continues to execute well – can create a balanced investment mix.

“Similarly, in the insurance sector, Old Mutual is undergoing a transformation under new leadership. The market awaits the first set of targets from the new management team, and we’re optimistic there’s significant upside potential given the low valuation base.

Read: Kokkie Kooyman’s outlook for SA’s banking sector

“Combining this with exposure to Discovery, which has developed a robust banking offering and aims for mid-teens earnings growth, can deliver strong returns over the next three years,” says Hechter.

Overall, Anchor believes that fund managers and private investors will shift toward domestic-focused companies, which should drive returns from SA equities over the next 12 months.

Read: Are gold shares overdone, or is this just the start of a bull market?

Follow Moneyweb’s in-depth finance and business news on WhatsApp here.