The answer is structural. A PMS can hold fewer than 20 stocks with very high concentration levels, sit on huge piles of cash when a manager sees no opportunity, or build a fixedincome portfolio around one client’s tax situation. It can also invest in corners of the market that large funds have effectively outgrown: micro-cap companies where even a small allocation would swallow a significant chunk of tradeable shares, or heavily focused on listed real assets through REITs (Real Estate Investment Trusts) and InvITs (Infrastructure Investment Trusts).

The strategy menu

R. Pallavarajan, Founder of PMS Bazaar, a PMS research and distribution platform, provides a lowdown on differentiated strategies that fall outside the mutual fund structure entirely. “Unlike mutual funds, PMS managers have the flexibility to run concentrated portfolios, take meaningful active cash calls, and customise portfolios at the client level. This allows them to pursue investment strategies that may not be practical within a mutual fund framework, particularly where liquidity, concentration, or portfolio customisation is involved.”

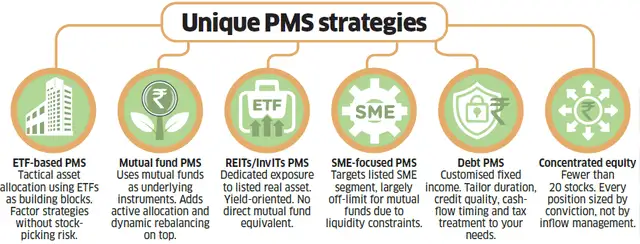

ETF-based PMS strategies construct portfolios predominantly using ETFs to enable tactical asset allocation and factor-based strategies. Mutual Fund PMS products use mutual funds as building blocks while layering active allocation and dynamic rebalancing on top. The strategies focused on REITs and InvITs offer dedicated, yield-oriented exposure to listed real assets, an asset class with no equivalent in the standard mutual fund catalogue. SME-focused strategies target segments that remain largely inaccessible through mutual funds due to liquidity and scale constraints.

Debt PMS products offer customised fixed-income portfolios calibrated to individual duration, credit quality and tax needs, something standardised debt funds cannot provide. At the equity end, deeply concentrated mandates hold fewer than 20 stocks, placing them in a category with no mutual fund parallel. “The differentiation in PMS,” says Pallavarajan, “is often less about finding entirely new asset classes and more about the ability to implement niche themes, concentrated strategies, tactical allocation decisions, and customised portfolio construction in ways that are not feasible within the mutual fund structure.

The micro-cap edge

Perhaps the most discussed structural advantage of PMS is its access to micro-cap and small-cap opportunities that large mutual funds have been priced out of by their own scale. Gurvinder Juneja, Principal Officer of Fortuna Asset Managers, spells it out: “A company with a Rs.600 crore market capitalisation and 45% public float has roughly Rs.270 crore of tradeable shares. A Rs.400 crore PMS taking a 3% position needs Rs.12 crore, which is achievable. A Rs.6,000 crore mutual fund taking the same position would need Rs.180 crore, 67% of the entire free float. This would move the stock against the fund’s own entry. Discipline about AUM is, at its core, a form of fiduciary responsibility.”

Aditya Agarwal, Co-founder of Wealthy. in, a wealth management platform for mutual fund distributors, agrees but draws a distinction: “A focused, small PMS can take and hold a concentrated micro-cap position and exit before scale bites. The edge is contingent on the PMS remaining small: a micro-cap PMS that aggressively gathers assets inherits the same liquidity ceiling.

The edge belongs to size discipline, not the PMS label.” Juneja adds a note of caution: “The micro-cap edge isn’t about how small the company is. It’s the manager’s own research feeding the client’s return, with nothing diluting it. The moment a lot of money piles up in the same stock, that link starts to weaken.”

When scale is the enemy

Every PMS strategy has a capacity limit, a point beyond which the approach that generated alpha begins to destroy it. Nehal Mota, Co-founder of Finnovate, provides a framework—micro/nano-cap strategies typically encounter friction at Rs.2,500-4,000 crore, where impact costs make deployment impossible without driving up entry prices. Special situations and arbitrage strategies face limits at Rs.3,000-5,000 crore because corporate action profit pools are fixed in size and additional capital dilutes returns. Concentrated mid-cap strategies may survive till Rs.7,500-10,000 crore before managers are forced to expand from 15 to 40-plus stocks, turning a high-conviction portfolio to one resembling an index fund.

Agarwal offers a simpler diagnostic: “There’s no single number; it depends on the liquidity of names the strategy must own. Warning signs are rising stock count, drift up the cap curve, falling active share, and returns hugging the benchmark.”

Strategies that depend on information edge and early entry, deep research requiring site visits, supply chain mapping, and promoter history remain the province of small, focused capital pools. Once size forces a manager into widely owned, efficiently priced names, the structural advantage evaporates.

What can a PMS do that a mutual fund can’t?

Concentrate: Run 15-20 stock portfolios with 8-10% in a single name.

Customise: Build around your tax position, sector exclusions, ESOP exposure.

Go Illiquid: Enter micro caps and special situations that large funds cannot touch without moving the price.

Supermarket vs chef

India’s mutual fund industry manages over Rs.80 lakh crore in assets across more than 50 asset management companies, with more than 2,000 mutual fund schemes. “A mutual fund house has become the financial equivalent of a supermarket, where every shelf is labelled differently, but everything is largely the same; the Nifty 50, repackaged 47 different ways,” says Manish Bhandari, Founder and CEO of Vallum Capital Advisors.

Not everyone shares the PMS industry’s scepticism of mutual funds. Himanshu Pandya, a Securities and Exchange Board of India (Sebi)-registered investment adviser, who has worked across both mutual fund and PMS industries, including as head of PMS business at ICICI Securities, questions the premise of PMS differentiation. “There’s no PMS strategy that a mutual fund cannot provide,” he says. For Pandya, the structural disadvantage of PMS on taxation compounds the problem. “A PMS isn’t tax-friendly. Even a single churn results in tax liability for the client, but infinite churns in a mutual fund don’t. If you were to manage funds in PMS and mutual fund structures—the same fund manager, same intelligence and same strategy would underperform in PMS by at least 100-350 basis points. It is a deficiency of the vehicle itself.”

Bhandari also highlights the risks. “Usually, investors go overboard and ask for a high-conviction three-stock or fivestock portfolio without understanding the risk. Such risks are very conveniently ignored in bull markets.” PMS, as per experts, is structured differently at its core. Unlike mutual fund investors, who hold units in a pooled vehicle, PMS clients hold securities in their own demat accounts. This structural difference cascades into various investment possibilities that mutual funds can’t replicate.

What PMS can do

The most important structural difference is concentration. Sebi limits mutual fund single-stock exposure to around 10% of net assets and mandates minimum stock counts across categories. A PMS is free from these constraints. Says Agarwal of Wealthy.in: “A PMS is not bound by mutual fund diversification rules and the minimum stock count, the single-stock cap, and the category equity exposure floors. So it can consistently hold a portfolio of, say, 25 stocks and 8-10% in one name. It also enables individual-level tax harvesting and customisation, and deploy in illiquid small companies that a large fund cannot touch without moving the price.”

Juneja of Fortuna Asset Managers frames the same point in terms of managerclient alignment. In a 70-stock mutual fund, the manager’s best idea accounts for 3-4% of the portfolio. In a concentrated PMS of 15 stocks, each high-conviction position can account for 8-12%. “The real advantage isn’t the rules a PMS skips. It’s that the manager’s best idea and the client’s goal can finally sit in the same portfolio, in a size that actually matters,” he says.

The flexibility extends beyond concentration. An actively managed equity mutual fund is structurally disincentivised from holding high cash balances due to style-drift rules and benchmark-tracking pressures. A PMS can move to 30-40% cash during market excess, a tactical lever that mutual funds cannot pull without consequence. Mota of Finnovate adds a size dimension: a `5,000 crore strategy trying to build a 5% position needs `250 crore of exposure, enough to distort pricing in a micro cap with limited free float, inflating entry costs and destroying the very alpha it was chasing.

This freedom also removes protection. The diversification limits, concentration caps, and market-cap floors that mutual fund investors never think about, are exactly what a PMS does away with.

The exclusivity trap

Customisation, a much-marketed feature of PMS, tells a similarly nuanced story. “Both exclusivity and customisation play a key role in driving demand for PMS. Positioned between mass-market MFs and more exclusive private equity, PMS appeals to HNI clients through its higher entry threshold, creating a sense of privileged access. Clients perceive PMS as a gateway to differentiated, high-quality ideas, driven by high-conviction investing and direct engagement with portfolio managers,” says George Heber Joseph, CEO and CIO, ASK Investment Managers.

Juneja frames customisation as a fiduciary question: “A good manager doesn’t just chase returns. He considers what the client keeps after tax and his big picture: ESOPs (employee stock option plans), existing exposure to their own industry, and tax situation, not just the slice of money in the PMS.”

Not all PMS growth is driven by investment logic. Says Juneja: “Nearly 35-40% people buy PMS for the wrong reasons, be it the distributor’s push, or the belief that a Rs.50 lakh entry must be better than those with a lower threshold. Exclusivity on its own isn’t a premium product. It’s the premium price for an ordinary one.”

Are you paying for alpha or exclusivity?

REASONS TO BUY PMS

- Concentrated portfolios.

- Tax-aware investing.

- Special situations.

- Direct ownership.

- Customised mandates.

RED FLAGS

- Exclusive’ but identical portfolios.

- Massive AUM in micro-cap strategies.

- Too many stocks.

- No capacity limits.

- Strategy resembles a mutual fund.

Red flags to watch out for

Even those who believe in PMS as a structure express concern about proliferation in recent years. Mota identifies overcrowding in thematic strategies as the biggest worry—several PMS funds continue raising capital despite operating in capacityconstrained segments. A Rs.10,000 crore ‘small-cap’ strategy behaves differently from a Rs.1,000 crore one, and investors are often unaware that the strategy they bought into has fundamentally changed as assets have grown. As Agarwal puts it: “Stress-test data shows that the largest small-cap funds need many weeks to liquidate even half their portfolios; at that size, a fund holds much of the small-cap universe, and its returns converge to the index, plus a fee. This is a structural ceiling, not a skill problem.”

Juneja identifies three categories of misalignment risk—momentum strategies that use fancy language, but whose portfolio construction does not match the marketing; thematic strategies launched at peak narrative, when asset-gathering incentives drive product launches at prices that cannot deliver returns; and managers who have outgrown their strategy’s capacity and are now using client assets to fund a business model rather than a genuine investment approach.

Investor takeaway

Sebi’s introduction of the Specialised Investment Fund (SIF), a new vehicle with a Rs.10 lakh entry threshold that permits long-short strategies, is set to reshape the industry. Says Mota: “The PMS industry is being forced upstream. Discretionary PMS providers will have to pivot away from generic long-only equity portfolios toward specialised, capacity-constrained strategies to justify their Rs.50 lakh entry barrier against lower cost SIFs. The long-term edge may belong to managers with differentiated research capability rather than distribution strength.”

Agarwal sees the same pressure playing out across three shifts: the new vehicle absorbing default PMS flows, a sharper split between trueedge strategies and commodified large-cap offerings, and greater sophistication through quant mandates, long-short approaches and GIFT City structures. ASK Investment Managers foresees the industry evolving toward an institutional-grade framework akin to global Separately Managed Accounts, combining niche public-market strategies with selective private-market access for UHNI clients. “PMS could emerge as the preferred vehicle for personalized investing among India’s affluent and ultraaffluent segments, transitioning from a tactical, high-return offering to a trusted long-term wealth solution,” says Joseph.

So the PMS world has two halves. One offers genuinely different products: a fund that buys only REITs, one that hunts in the SME space, a tiny fund holding a handful of micro-caps that a big fund couldn’t touch. The other offers products behaving like mutual funds once you look past the price tag. The PMS advantage is real, but it’s not in the label. It’s in specific strategies, run by managers who keep their fund small enough to stay nimble, and care more about getting it right than collecting more money.