Abstract

This paper examines trader behaviour within the Axi Select framework, focusing on how position sizing, rather than strategy selection, determines survival and progression. Using a $500 entry account as the baseline, we analyze how different risk-per-trade models interact with drawdown constraints, market volatility, and trade sequencing. The findings show that while a higher risk (5% to 10%) can accelerate outcomes, it materially reduces the probability of passing the evaluation phase. In contrast, a controlled risk framework of 1%-2.5% maximizes the trader’s ability to survive volatility and complete the required trade sequence. The conclusion is clear: in Axi Select, the edge is not what you trade, but how much you risk while trading it.

1. The Axi select reality: You are being tested on survival

Axi Select is often approached as a trading opportunity.

In reality, it is a risk management test disguised as a trading program.

The structure implicitly rewards:

- Consistency over aggression.

- Discipline over conviction.

- Survival over short-term performance.

This creates a mismatch between how traders want to trade and how they must trade to progress.

2. The $500 constraint: Small capital, big consequences

With a $500 starting balance, every decision is magnified.

At this scale:

- 1% risk = $5.

- 5% risk = $25.

- 10% risk = $50.

This matters because the effective failure threshold is typically in the range of 10% drawdown.

Which means:

The account is not designed to absorb mistakes — it is designed to expose them.

3. The core trade-off: Speed vs survival

There are two distinct ways to approach Axi Select:

Path A: High Risk (5%–10%)

- Faster P&L swings.

- Potential for rapid progression.

- Extremely sensitive to loss sequencing.

Path B: Controlled Risk (1%–2.5%)

- Slower growth.

- Higher consistency.

- Greater tolerance for variance.

The key insight:

Axi Select rewards completion of the process, not speed through it.

4. Variance compression in Axi select

At elevated risk levels, traders experience variance compression.

At 10% risk:

- 1 loss = -10%.

- 2 losses = -19%.

At 2.5% risk:

- 3 losses = -7.3%.

- 5 losses = -12%.

In Axi Select terms:

- High risk reduces the number of allowable errors to near zero.

- Moderate risk allows the trader to complete the required trade sequence.

5. The “Not behind the 8 ball” argument — and Why It still fails

It is technically correct that:

One 10% loss does not place the trader at an immediate disadvantage.

However, Axi Select is not a single-trade game.

It is a multi-trade consistency test.

After one large loss:

- Risk tolerance collapses.

- Psychological pressure increases.

- Trade selection becomes distorted.

The trader is not mathematically impaired, but is operationally constrained

6. Market regime matters: Why now is the hard mode

Current conditions are defined by:

- Oil-driven volatility.

- Geopolitical headline risk.

- Cross-asset instability.

In this regime:

- FX behaves less predictably.

- Stops are more likely to be triggered by noise.

- Correlations break down.

Which leads to a critical adjustment:

A 2.5% risk in this environment can behave like 4% or more in normal conditions

7. The 20 trade reality: Process over outcome

Axi Select requires a sequence of trades.

This transforms trading into:

- A process completion exercise.

- Not a single high-conviction opportunity.

The implication:

Traders must optimize for consistency across trades, not magnitude within trades

A structured approach, such as a 20-trade test phase, becomes essential for:

- Measuring discipline.

- Validating execution.

- Managing emotional variance.

8. Recommended framework for axi select

A practical structure aligned with survival and progression:

Risk Allocation

- Base trades: 1%.

- High-conviction trades: 2% to 2.5%.

- Absolute maximum: 3%.

Execution Rules

- 1 to 3 trades per day.

- Pause after two consecutive losses for an interday time out.

- Predefined stop loss on every trade (I will discuss that in another blog post).

Market Selection

- Focus on:

-

- EUR/USD.

- USD/JPY (with yield awareness).

- AUD/NZD.

- Avoid:

-

- Oil-sensitive pairs.

- Highly reactive instruments during geopolitical spikes.

9. When not trading is the trade

One of the most underutilized edges in Axi Select is selectivity.

In unstable regimes:

- The signal-to-noise ratio deteriorates.

- False moves increase.

- Execution quality declines.

Choosing not to trade is not inactivity.

It is risk preservation

10. Conclusion: The trader who lasts, passes

Axi Select does not reward the most aggressive trader.

It rewards the trader who:

- Maintains discipline under constraint.

- Survives variance.

- Completes the process.

The central takeaway is this:

In Axi Select, position sizing is the strategy.

Everything else is secondary.

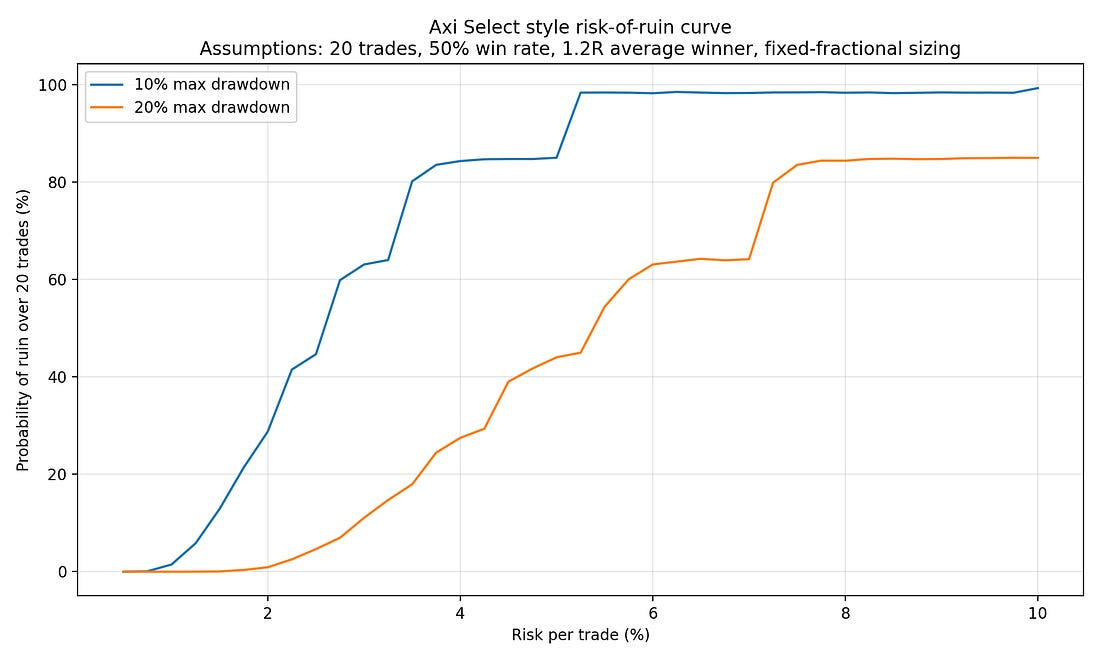

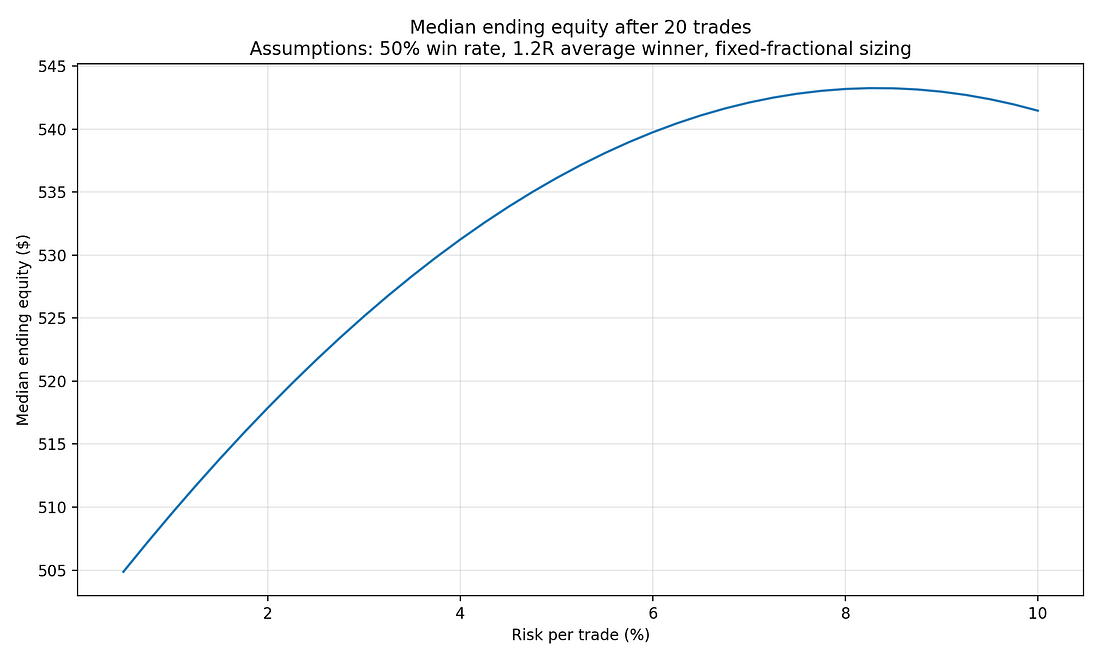

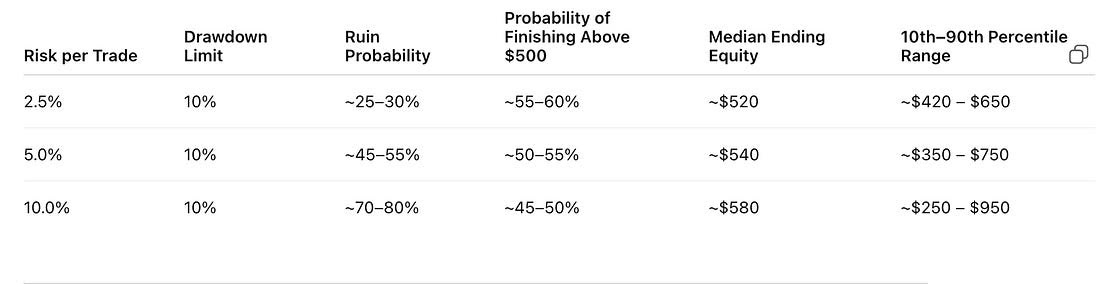

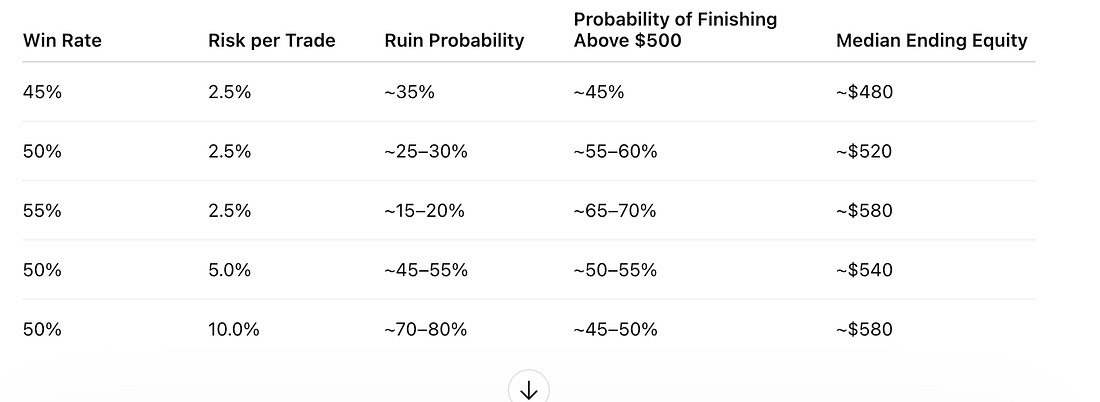

Risk of ruin across position sizing (Axi select framework)

Assumptions: 20 trades, $500 starting equity, 50% win rate, 1.2R average winner, fixed fractional risk model

Sensitivity to Win Rate (10% Drawdown Limit)

Key assumption set:

20 trades, $500 starting equity, fixed fractional sizing, 50% win-rate baseline, 1.2R average winner, with ruin defined as breaching a maximum drawdown threshold.