The inflation rate has been slowing down this year. It grew at a 2.4% annualized rate in February, down from 2.7% last year and a peak of 7% in 2021. However, with oil prices surging due to the war with Iran, inflation could reaccelerate.

Here’s a look at whether gold and silver streaming company Wheaton Precious Metals (WPM 0.83%) is a good inflation hedge.

Image source: Getty Images.

Precious metals as an inflation hedge

Precious metals such as gold and silver have traditionally been good inflation hedges. That’s because they’re finite resources that are globally recognized. Investing in gold tends to be a better inflation hedge because it offers more stability and resilience than silver. It also has strong demand from central banks, which use it as a store of value.

Silver can also be a good inflation hedge. However, it’s more volatile. Silver also has greater growth potential due to its importance as an industrial metal for products such as solar panels and electronics.

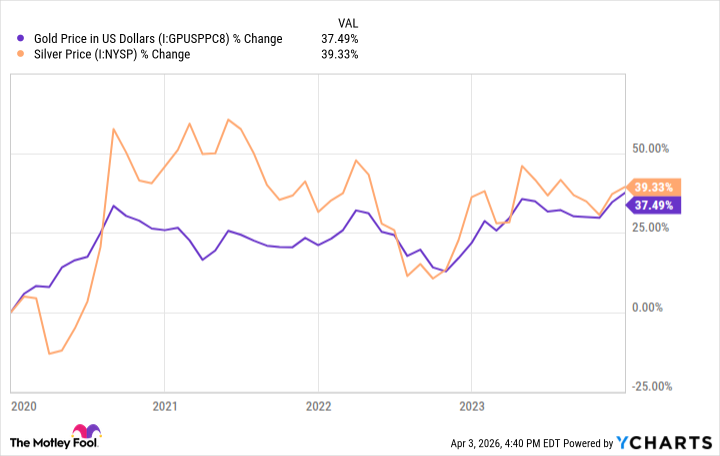

Here’s how the two precious metals performed during the period of high inflation caused by the pandemic:

Gold Price in US Dollars data by YCharts

Wheaton’s inflationary benefits

Wheaton Precious Metals doesn’t mine silver and gold. The streaming company provides capital to miners to develop and expand mines. In exchange, it receives the right to a portion of their production at a set price. The company has locked in fixed costs of $650 per ounce for gold and $2.50 per ounce for silver through 2030. As a result, it has predictable costs with no inflationary cost pressures. That enables it to cash in on the upside of silver and gold prices during inflationary periods.

Today’s Change

(-0.83%) $-1.14

Current Price

$135.66

Key Data Points

Market Cap

$62B

Day’s Range

$129.61 – $137.38

52wk Range

$68.03 – $165.76

Volume

118K

Avg Vol

2.6M

Gross Margin

72.17%

Dividend Yield

0.51%

In addition to those low fixed costs, Wheaton benefits from the growing production of its mining partners. The company currently expects its gold equivalent ounces to rise 11% this year and by 50% by 2030 based on recently acquired streams and mining developments by its partners. Wheaton has ample financial capacity to fund new streams that could enhance its already robust growth rate. This rising production should drive earnings and cash flow growth even if precious metals prices stagnate. That supports the company’s plan to continue paying a progressive dividend (it recently hiked its payout by 18%).

A great inflation hedge

Wheaton Precious Metals’ combination of inflation-protected costs, upside to higher precious metals prices, and production growth has enabled it to consistently outperform silver and gold. As a result, it has historically been an even better hedge against inflation than precious metals.