Weather: If the market is the barometer, US wheat conditions have been efficiently priced in and, now, consideration is being given to better areas offsetting poorer areas. There is no doubt the western belt is poor and parts of the SRW belt are now arguably too wet – however, the real test will be when the wheat tours start kicking some dirt.

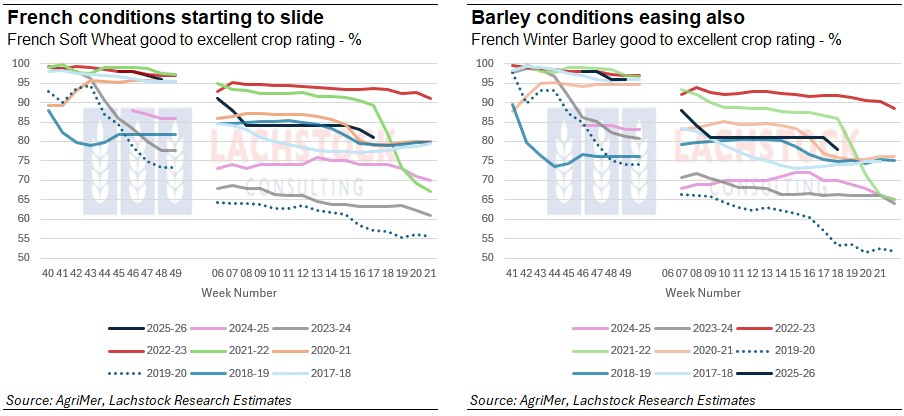

French conditions finally showed signs of some crop stress, although its from a very high base relative to other years. Harvest will kick off in around 2 months so the fact there is a bunch of rain forecast should stop the bleeding.

Markets

The efficiency of ag futures markets to converge to physical markets is pretty good compared with other commodity markets. So the fact that a few big grain companies delivered grain onto the futures market should tell you that futures are now above cash — and as last night shows you, that should also tell you where the path of least resistance lies. Historically, deliveries onto futures have tended to mark a ceiling for rallies, as the arbitrage between cash and futures gets worked out in the most blunt way possible. That said, this is far from a closed chapter — there is a long season ahead and the upcoming wheat tour has consistently been a source of significant price volatility, meaning fresh fundamental information could quickly reopen the debate.

Crude touched its highest point since the Iran debacle started – and Donald is sticking fat. From an Ag commod perspective the China meeting is arguably more important.

Day Ahead – Australia

Given that Russian cash didn’t move and that US futures have not really been linked to Australian export prospects, last nights down move shouldn’t matter – but it probably will.

AUD the sunny side of 0.7200 will keep things in check. I ponder this a lot lately – The carry trade is keeping the AUD supported – Aussie rates are firming against the US, so the AUD catches a bid. However, you dont have to pick too hard at the threads to see that not all is that rosy down here. Jim is about to deliver an absolute stinker of a budget, Victoria is a special kind of broke and cost of living.

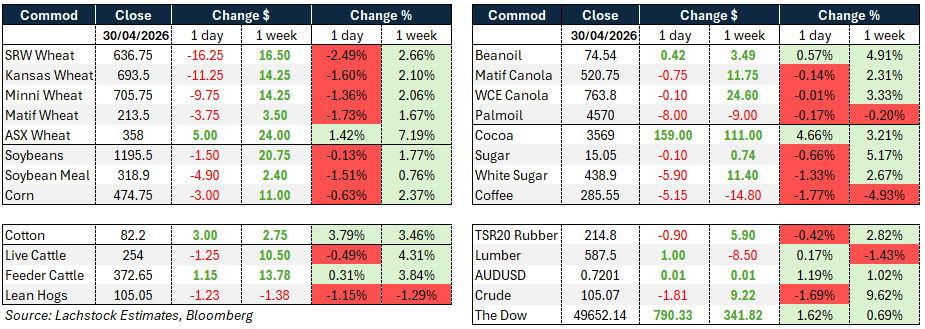

Global wheat: Chicago July -16.25c, Kansas July -11.25c, Matif Sep -€3.75

Global wheat: Chicago July -16.25c, Kansas July -11.25c, Matif Sep -€3.75

Wheat markets pulled back sharply, closing out a strong April on a soft note after surprise deliveries from Bunge (578 HRW) and The Andersons (400 Chicago) caught the market off guard given recent basis strength and cancellations.

Month-end positioning added to the selling pressure.

The market narrative is shifting — having been fixated on HRW production cuts, traders are now questioning whether better areas of the southern plains can offset the parched west, whether demand losses are outpacing production losses, and whether Chicago will trigger a storage expansion in July if WN/WU spreads remain weak. VSR talk for July has emerged.

Russian cash was quoted at $241 and French Rouen exports fell week on week to 90,216 tons.

US old crop wheat sales came in at 226k tons versus 150k expected, with Indonesia taking 40k HRW and 30k WW. Indonesia is also tightening import rules, requiring agriculture ministry endorsement before purchases, as President Prabowo pushes toward food self-sufficiency.

Poland’s winter grain area rose 1.1% to 4.5 million hectares.

Egypt’s domestic procurement is running 13% ahead of the same period last year.

Some market participants view wheat as overpriced given the global supply picture, with US values seen as uncompetitive on export markets.

Crop tours are set to begin soon and should provide more precise production detail.

Other grains and oilseeds: Corn-3c, Soybeans July -1.5c, Matif Canola Jul -C$0.10

Corn came within a quarter cent of 500 before retreating, finishing down 3.5c at 494.25 as crude’s $1.81 decline removed a key support.

Weekly corn sales of 1.598 million tons beat expectations of 1.45 million, with Colombia the top buyer.

Argentina’s corn harvest reached 28% complete and Argentine corn is approaching the cheapest fob value globally, which should pressure cash prices as harvest accelerates.

Brazil’s safrinha remains mostly dry outside of Parana, which has seen some relief.

Soybeans were mixed with the July contract slipping 1.5c while the November gained 1.75c; meal lost $4.90 and bean oil rallied 42 points, leaving July crush down 4.75c at 326. Soybean sales of 258k tons missed the 400k estimate though meal and oil sales were near or above expectations.

End-of-month rolling lifted July’s share of the flat price to 53.9%.

Argentine soy harvest advanced to 18.3% from 10.2% the prior week. ICE canola settled mixed with old-crop July slightly lower and new-crop months posting modest gains as the market consolidated following Wednesday’s rally.

Canadian crush data for March came in strong at 1.097 million tons, up 7% year on year, with the marketing year cumulative crush up 4%.

Biodiesel demand expectations remain supportive of vegetable oil markets broadly.

A stronger Canadian dollar weighed on crush margins.

The EU-Mercosur free trade agreement is set to be implemented Friday.

Bunge raised its outlook citing biofuels clarity, while Wilmar reported a 23% fall in first quarter core profit on hedging losses tied to Iran-related volatility.

Macro: AUD 0.7200, Dow +790.33, Crude -$1.81

The dominant macro theme remains the Iran war and the Strait of Hormuz closure. Brent briefly touched $126 a barrel, its highest since the conflict began in late February, before settling near $114, leaving prices up more than 8% on the week.

Trump reiterated support for the naval blockade, saying Iran’s economy is crashing, while Iran’s new supreme leader Mojtaba Khamenei vowed to retain nuclear and missile technologies and keep control of the strait.

US military commanders were briefed on strike options including a short wave of strikes to break the negotiating deadlock, with analysts at Bloomberg Economics suggesting renewed action is most likely within two weeks.

Retail gasoline in California has surpassed $6 a gallon and the national average is at fresh highs, creating political pressure ahead of midterm elections.

The energy crunch is accelerating biofuel interest as governments look to stretch fuel supplies.

On trade, US-China relations showed tentative signs of thaw ahead of Trump’s May 14-15 summit with Xi Jinping, with Treasury Secretary Bessent and USTR Greer holding a video call with Chinese Vice Premier He Lifeng, though China flagged serious concerns over US restrictive measures.

Meanwhile Beijing’s new trade rules, which could penalise companies shifting supply chains away from China, have drawn a muted response from Washington.

US Q1 GDP grew at an annualised 2%, beating expectations, supported by a 10.4% surge in business equipment investment driven by AI spending, though consumer spending at 1.6% was modest.

Kevin Warsh faces a hawkish FOMC as he prepares to take over as Fed chair amid entrenched energy inflation.

Ukraine peace talks remain stalled, with Zelenskiy citing the Iran conflict as a key distraction and warning against lifting sanctions on Russia in exchange for a short-term ceasefire around May 9 Victory Day.

Local: WA bids were stronger, with canola $800 current season and $850 new season, wheat $353 and $370, and barley $350 and $338 FIS Albany.

Through the east, markets were hot yesterday, with wheat and canola leading the way. Current season canola was $790 and new crop $830, wheat $350 and $370, and barley $316 and $332 track Geelong.

Delivered markets remain well bid, with Hanwood at $372 for July and $390 Jan+, trading slightly above Geelong/Melbourne ASW.

Lentil demand remains hand-to-mouth for the most part, with bids around $690 delivered Vic ports/packers.