However, the reality is different.

According to a 2024 study by the Securities and Exchange Board of India (Sebi), over 91% of individual traders lost money in F&O (Futures and Options) trading in 2023-24. Even after regulatory reforms introduced in May 2025 to strengthen the equity derivatives framework, the proportion of loss-making traders remained unchanged, at 91% in 2024- 25. This highlights the structural challenges retail traders face when dealing with complex instruments like options.

Although futures and options are often grouped together, their risk characteristics differ substantially:

- Futures contracts obligate the buyer and seller to transact at a predetermined price on a future date, which exposes traders to unlimited risk.

- Options contracts, on the other hand, give the buyer the right but not the obligation to buy or sell an asset at a specific price within a defined time frame. The buyer pays a premium for this right, and the maximum loss is capped at the premium paid.

This built-in cap makes options appear safer for buyers compared to futures. Yet options are far more complex because their pricing depends on multiple variables beyond simple market direction. Without a solid understanding of these dynamics, retail investors often find themselves speculating rather than strategising.

The first part of this two-part series explores two key concepts every options trader must understand—moneyness and the components of option pricing.

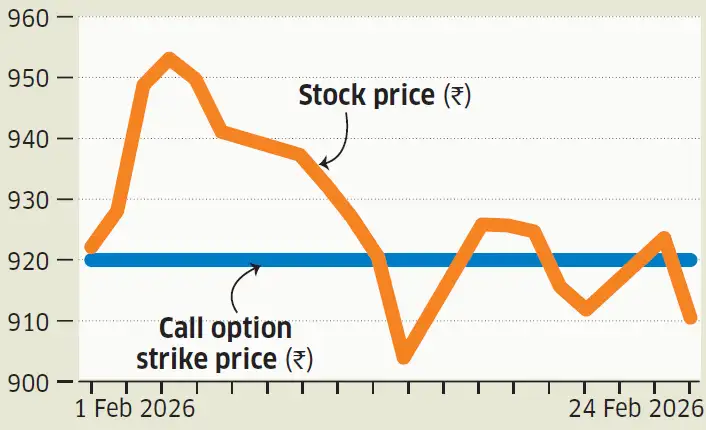

Stock price vs call option strike price

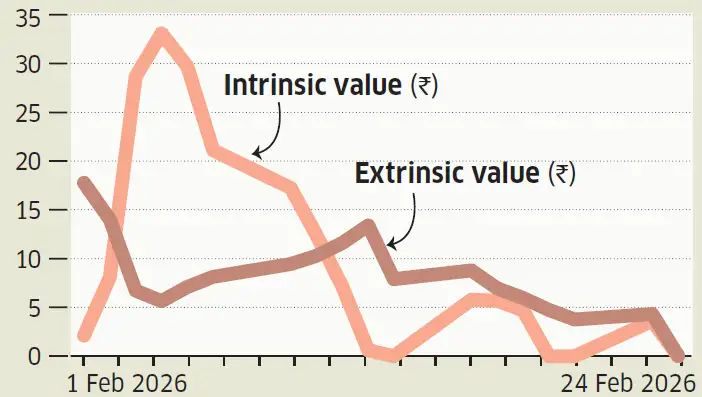

Call option premium: Intrinsic and extrinsic value

What are options?

An option is a standardised financial contract that grants the buyer the right, but not the obligation, to buy or sell an underlying asset—such as the Nifty 50 index or a stock—at a predetermined price (called the strike price) within a specified period.

- The buyer pays a premium (the option price) to acquire this right.

- Options are traded in lot sizes, meaning each contract represents a fixed number of shares of the underlying asset. For example: Nifty 50 index options have a lot size of 65. Bank Nifty options have a lot size of 30. There are two basic types of options:

- Call options: Gives the right to buy the asset; useful when the outlook is bullish.

- Put options: Gives the right to sell the asset; useful when the outlook is bearish.

If the market moves against the buyer’s expectation, the option expires worthless, and the buyer loses the premium paid. Thus, the risk for buyers is limited and known in advance. On the other side are option sellers (or writers), who receive the premium and take on the obligation to buy or sell the underlying asset if the option is exercised. While the seller’s profit is limited to the premium received, the potential losses can be substantial if the market moves sharply against their position.

It is entirely possible for an investor to correctly predict the direction of the market and still lose money in options trading. A key reason is the lack of understanding of how option premiums are structured and how they evolve over time.

Are you winning yet?

Moneyness tells you whether your option is making money.

Retail traders prefer OTM options because of their lower prices.

Components of option premium

An option’s price or the premium is not a single number; it is the sum of two distinct parts: Intrinsic Value and Extrinsic Value.

1. Intrinsic Value (real value): This is the “real” or “tangible” value of the option. It represents the profit that could be realised if the option was exercised immediately.

- For call options: Intrinsic Value = (Current Stock Price – Strike Price). If this is negative, the intrinsic value is zero.

2. Extrinsic Value (time value): This is the “hope” factor. It represents the additional amount traders are willing to pay for the possibility that the option will become more profitable before it expires.

- Extrinsic Value = Total Premium – Intrinsic Value.

Time decay factor: A crucial feature of extrinsic value is that it declines as the option approaches expiration. This gradual erosion of time value is known as time decay. If the underlying asset does not move significantly, the option’s extrinsic value shrinks day by day, causing the option price to fall even when the index price remains unchanged.

On 1 February 2026, a call option for a large private sector bank stock with a strike price of Rs.920 was trading (option price) at Rs.19.8. At that time, the stock was at Rs.922.1.

- Intrinsic Value: Rs.2.1 (The immediate benefit of buying at Rs.920 vs Rs.922.1)

- Extrinsic Value: Rs.17.7 (19.8 minus 2.1; the “premium” for time). By 23 February, the stock had barely moved, closing at Rs.923.6. However, the option price had fallen to Rs.7.5 due to time decay (because time passed and the ‘hope value’ kept shrinking). On the final expiry day (24 February), the stock closed at Rs.910. Because the stock price was now below the strike price, the option expired at Rs.0, resulting in loss for the buyer (Charts on left).

In many cases, investors buy options that consist largely of extrinsic value. Unless the underlying asset moves strongly and quickly enough to generate intrinsic value, the erosion of extrinsic value can outweigh any gains, leading to losses.

Option moneyness

Understanding moneyness is critical for understanding why retail traders lose money. Moneyness refers to the relationship between the strike price and the current market price of the underlying asset. In simple terms, moneyness tells you how close your option is to making money.

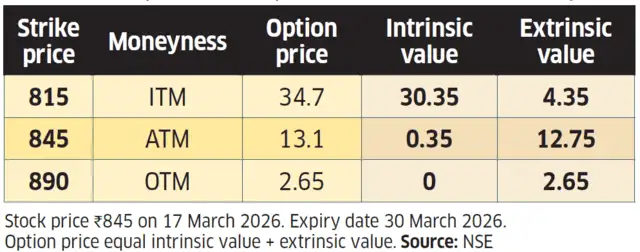

In-the-Money (ITM): For call options, the strike price is below the current market price. These have high intrinsic value and a higher probability of profit, but they are expensive to buy.

At-the-Money (ATM): The strike price is equal to or very near the current market price. These options are highly sensitive to price changes but carry the highest amount of extrinsic (time) value.

Out-of-the-Money (OTM): For call options, the strike price is above the current market price. These have zero intrinsic value and consist entirely of extrinsic value.

Consider call options of the same large private sector bank with a stock price of Rs.845.35 with expiry date of 30 March 2026 (left below).

Many retail traders incline toward OTM options because they are cheap. The low premium makes them appear attractive, and the potential percentage returns can be enormous if the market moves sharply. However, the probability of profit is low.

OTM options are essentially lottery tickets:

- They have no intrinsic value.

- Their entire worth is based on extrinsic value, which decays rapidly.

- Unless the underlying asset makes a large move in a short time, these options expire worthless.

ATM options are highly pricesensitive but carry high time value (or extrinsic value), making them prone to time decay if the underlying doesn’t move quickly. ITM options are more likely to profit but require higher premiums.

Next week, the second and concluding part of this series will explore the ‘Option Greeks’—the forces that drive option prices—covering volatility, time decay, and the sensitivity of option values to movements in the underlying asset.