Last Updated:

Small savings schemes currently offer returns in the range of 4% to 8.2%, depending on the instrument. These returns are modest but reliable.

![]()

Investment in times of volatility

Periods of geopolitical tension—whether conflicts in the Middle East, trade wars, or currency volatility—tend to rattle financial markets. Equity indices turn volatile, risk appetite weakens, and investors begin to reassess portfolio allocation. In such an environment, the debate between the safety of small savings schemes and the growth potential of equities becomes more relevant.

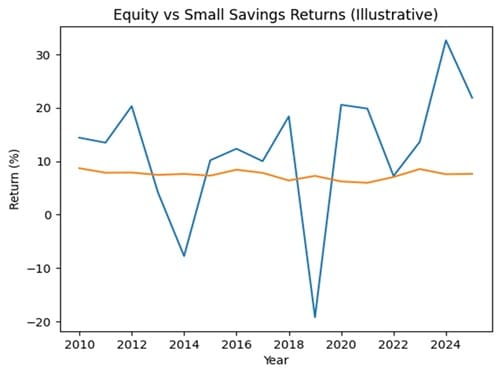

Stability vs Volatility

Small savings instruments such as the Public Provident Fund (PPF), National Savings Certificate, and post office deposits offer stability backed by sovereign guarantee. Returns are fixed, predictable, and insulated from market swings—making them particularly attractive during uncertain times.

Equities, on the other hand, are inherently volatile. Geopolitical shocks often trigger sharp sell-offs, especially in sectors linked to global trade, commodities, or currency movements. While such corrections can create buying opportunities, they also expose investors to short-term losses.

Return Trade-off

The trade-off is clear: safety versus higher potential returns.

Small savings schemes currently offer returns in the range of 4% to 8.2%, depending on the instrument. These returns are modest but reliable.

Equities, historically, have delivered higher long-term returns—often in the low double digits—but with significant interim fluctuations. During periods of uncertainty, returns can be negative in the short term.

| Factor | Small Savings | Equities |

|---|---|---|

| Return Potential | Moderate (4–8.2%) | High (10–14% long-term) |

| Volatility | Very Low | High |

| Downside Risk | Minimal | Significant in short term |

| Liquidity | Low–Moderate | High |

| Tax Efficiency | High (80C, EEE in PPF) | Depends on LTCG/STCG |

Liquidity and Investment Horizon

Liquidity is another key differentiator.

Most small savings schemes come with lock-in periods. For instance, PPF has a 15-year tenure, while NSC typically locks funds for five years. This makes them suitable for long-term, goal-based investing but less flexible.

Equities offer far greater liquidity, allowing investors to enter and exit positions quickly. However, this flexibility can also lead to impulsive decisions during volatile phases.

Behavioural Advantage

In times of geopolitical stress, investor behaviour often becomes risk-averse. Small savings schemes help counter this by enforcing discipline through fixed tenures and guaranteed returns.

Equity investing, in contrast, requires emotional resilience. Investors who panic during downturns risk locking in losses, while those who stay invested may benefit when markets stabilise.

Portfolio Strategy: Balance is Key

Rather than choosing one over the other, a balanced approach is often more effective.

Small savings schemes can act as the “anchor” of a portfolio—providing stability and predictable income—while equities can drive long-term wealth creation.

In periods of heightened uncertainty, investors may consider increasing allocation to fixed-income instruments while continuing systematic investments in equities to benefit from market corrections.

Geopolitical uncertainty doesn’t eliminate opportunities—it reshapes them. Small savings schemes offer safety and certainty when markets turn volatile, while equities continue to reward patience over the long run.

The optimal strategy lies not in timing the market, but in aligning investments with risk tolerance, time horizon, and financial goals.

March 31, 2026, 10:22 IST

Read More